REIT Glossary

Accretive Acquisition

- Sometimes also referred to as “yield-accretive acquisition”, an accretive acquisition is the purchase of an asset that leads to an increase in the acquiring S-REIT’s distribution per unit.

- The opposite of an accretive acquisition is a dilutive acquisition (see below)

Acquisition Fee

- A fee paid to the S-REIT manager by the S-REIT to compensate the S-REIT manager for its efforts and expenses associated with acquiring a new property.

Aggregate Leverage

- Also known as “gearing”, it is the ratio of a REIT’s debt to its total deposited property value. In Singapore, S-REITs have a gearing limit of 45%.

Anchor Tenant

- The term used to describe the lessee that rents a significant (generally the largest) portion of a property.

- Anchor tenants usually sign long-term leases which allows them to negotiate favourable lease agreements with the S-REIT or property manager, as finding a replacement anchor tenant can be challenging.

- Properties with large numbers of anchor tenants thus usually have long weighted average lease expiry (WALE).

Ancillary Tenant

- The term used to describe the lessee that does not rent a significant portion of a property.

- Ancillary tenants are usually smaller businesses that rent smaller lots with generally shorter-term leases.

- Ancillary tenants may have lesser bargaining power than anchor tenants and may thus have to settle for less favourable lease terms

- Tenant turnover is generally higher among ancillary tenants than anchor tenants

- Properties with disproportionately higher numbers of ancillary tenants tend to have shorter weighted average lease expiry (WALE).

Base Fee

- A fee that the REIT pays to its REIT managers regardless of the performance of the REIT (usually in the range of 0.1% – 0.5% of the total assets of each REIT).

Base Rent

- The minimum amount of rent required to be paid by the tenant to the landlord, aside from other provisions such as overage rent.

- Base rent is typically subject to periodic increases (positive rental reversions) and ensures growth in operating income for the REIT.

CAPEX

- Short term for Capital Expenditures, CAPEX refers to costs incurred to acquire, maintain or upgrade assets such as properties, plants and equipment.

- These measures include asset enhancement initiatives (AEIs) to refurbish a building, lifts and escalators maintenance and property acquisitions.

Capitalisation Rate

- Capitalisation Rate = Property’s Net Operating Income/Purchase Price

- A measure indicating how well a REIT generates income through its operation of a particular property.

- High capitalisation rates indicate higher returns and greater perceived risk.

CIS Code – The Code on Collective Investment Schemes issued by the MAS

- The CIS Code is issued by the Monetary Authority of Singapore (MAS) pursuant to section 321 of the Securities and Futures Act (Cap. 289). The CIS Code sets out the best practices on management, operation and marketing of schemes that managers and approved trustees are expected to observe.

- The CIS Code is non-statutory in nature and a failure by any person to comply with any requirement in the CIS Code will not of itself render that person liable to criminal proceedings

- However, the MAS may take into account any non-compliance with the CIS Code in determining whether to revoke the authorisation or recognition of the scheme or to refuse to authorise new schemes to be offered by the same responsible person

- Appendix 6 of the CIS Code (the Property Fund Guidelines) contains detailed guidance on the rules to be observed by Singapore REITs.

Committed Occupancy

- Occupancy rate based on all current leases in respect of the properties including letters of offer accepted by tenants which are to be followed up with tenancy agreements to be signed by the parties and for which a small deposit fee has been paid.

Convertible Perpetual Preferred Units (CPPUs)

- Preferred units issued by a REIT that have no maturity or no specific buyback date, and include an option to allow the unitholder to convert them into a pre-determined number of common units.

- CPPUs give unitholders voting rights, but no claim on assets if the REIT folds. They are traded separately from common units of the REIT, albeit their prices will be based closely on the performance of the common stock.

Cost of Capital

- The cost to a company of raising capital in the form of equity (common and preferred stock) or debt.

- The cost of equity capital generally includes both the dividend rate and the expected equity growth rate (by higher dividends or stock prices).

- The cost of debt capital is the interest expense on the debt incurred.

Data Centre REITs

- REITs that invest primarily in properties that house data storage systems, computer systems and other associated components. These are typically highly specialised buildings, with provisions for climate control measures and backup power supplies.

- Data Centre REITs do not depend on a high volume of pedestrian traffic and are usually situated away from population centres (industrial areas). They have long and stable leases, where tenants are typically companies such as large IT firms.

- With the proliferation of smartphones and computers and the rise of digitalisation across various sectors, we could see more Data Centre REITS in the near future.

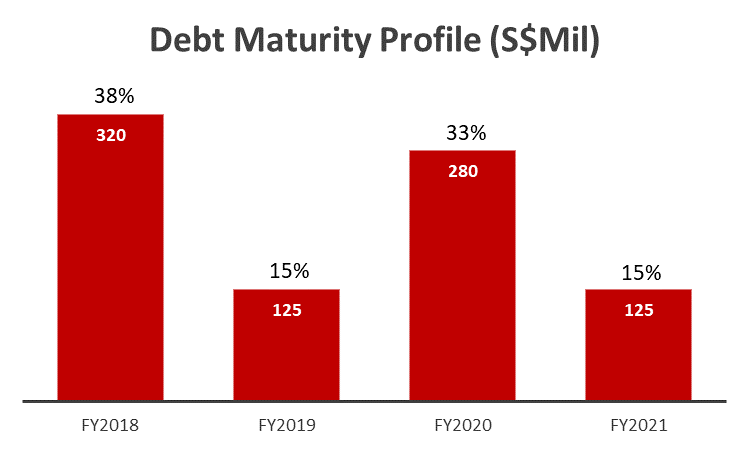

Debt Expiry Profile

- A schedule showing the expiry profile of the REIT’s debt by year.

This chart shows what percentage of a REIT’s total debt is slated to expire in any given fiscal year.

This chart shows what percentage of a REIT’s total debt is slated to expire in any given fiscal year.

Deposited Property

- The value of the REIT’s total assets based on the latest valuation.

Development Fee

- A fee charged by real estate developers for developing commercial properties for the REIT, typically as a percentage of the development cost.

Dilutive Acquisition

- A dilutive acquisition is the purchase of a property that leads to a reduction in the acquiring REIT’s distribution per unit.

- The opposite of a dilutive acquisition is an accretive acquisition (see above)

Distributable Income

- Net income subject to certain adjustments including adding back depreciation and amortization, future income tax expenses and excluding any gains or losses on the disposition of any asset, future income tax benefit and any other adjustments as determined.

Distribution per Unit (DPU)

- The amount of dividends a REIT investor receives for every unit he has in the REIT.

- DPU = Distributable Income/Total Number of Units Outstanding.

Distribution Yield

- Also known as Yield on Cost (YOC), Distribution Yield is a metric used to measure the performance of REITs.

- Distribution Yield = Dividend Payout/ market price of a unit in the REIT at the point of acquisition.

Earnings per Unit (EPU)

- The amount of earnings the REIT generates for every unit it has outstanding. This is different from Distribution per Unit (DPU), which is the amount of dividend payout a REIT investor gets for every unit he has in the REIT.

- EPU = Net Income/Total Number of Units Outstanding.

Fee

- Fee paid by a REIT to its REIT manager to compensate the REIT manager for its efforts and expenses incurred in selling part of a REIT’s assets or subsidiaries.

Fixed Rent

- Rental income received or receivable from tenants based on the fixed rent method, under which rent is at fixed pre-determined rates (after adjusting for leasing incentives such as rent rebates and rent-free periods where applicable).

Gearing

- Also known as Aggregate Leverage, it is the ratio of a REIT’s debt to its deposited property (total assets). In Singapore, S-REITs have a gearing limit of 50%. (On 16 April 2020 MAS raised the aggregate leverage limit for S-REITs from 45% to 50%)

Greenfield Development

- An expansion strategy or project in which a REIT manager decides to develop a new property or development from scratch.

Gross Floor Area (GFA)

- A metric indicating the total amount of space available within a building development including walls, corridors and columns.

Gross Rental Income

- Comprises Fixed Rent and Turnover Rent

Gross Revenue

- Total revenue collected from all of a REIT’s portfolio of assets (including gross rental income, car park income and other income).

Gross Turnover Rent

- Gross Turnover rent (GTO), is the extra rent payable by the tenant once its sales exceed a pre-set target. A typical GTO rent arrangement involves a base rent component and a deduction from total sales once it reaches the pre-set target.

Healthcare REITs

- REITs that specialise in various types of healthcare properties such as hospitals, nursing homes, medical centres and assisted living facilities for the elderly and disabled.

Hospitality REITs

- REITs that hold hospitality related properties and short-term accommodations such as hotels and serviced apartments.

Income Available for Distribution

- An S-REIT’s cash-on-hand that is available to be distributed to unitholders

- A measure of an S-REIT’s ability to generate cash and distribute dividends to its shareholders.

Industrial REITs

- REITs that are primarily involved in the acquisition, development, ownership, management and leasing of industrial properties such as factories, distribution centres and warehouses.

Lease Expiry Profile

- The percentage of tenant leases across the entire REIT’s portfolio that is slated to expire in any given year. This can be measured based on gross income or net lettable area.

Lease Novation

- A lease novation is when a tenant transfers its rights and obligations under the current lease agreement to a third party, before the expiry of the lease agreement. This novation must receive full consent from both the tenant and the landlord to be valid.

Net Asset Value (NAV)

- The net market value of all a company’s assets, including but not limited to its properties, less all its liabilities and obligations.

Net Lettable Area (NLA)

- A metric indicating the amount of floor space within a property that can be rented out for income.

Net Property Income (NPI)

- A metric used to determine a property portfolio’s profitability and financial health, less its operating and recurring expenses.

- Net Property Income (NPI) = Gross Revenue of a Property – Property Related Expenses (e.g. building maintenance)

Office REITs

- REITs that are primarily involved in the acquisition, development, ownership, management and leasing of office properties.

Perpetual Securities

- Hybrid securities issued without a maturity date. Perpetual securities share some of the features of both bonds and shares. Although they are often referred to as “perpetual bonds” and “perpetual notes”, they are not to be confused with conventional bonds.

- Issuers of perpetual securities usually offer to pay fixed distributions. However, unlike bonds, issuers of perpetual securities often have the discretion to stop paying distributions altogether without triggering a default. Perpetual securities have no maturity date, so they can continue to exist perpetually, unless they are redeemed by the issuer.

Property Management Fee

- The fee paid to the REIT’s appointed property manager (out of the assets of the REIT), to manage the underlying real estate properties of the REIT.

Property Manager

- A Property Manager is typically appointed by the REIT Manager to manage the underlying real estate properties of the REIT. It oversees renting out the property to achieve the best tenancy mix and rental income, running marketing events or programs to attract human/shopper traffic and to upkeep the property in general. In exchange, the Property Manager is paid a Property Management Fee out of the assets of the REIT.

Property Yield

- A metric used to assess the income-generating power a REIT’s portfolio of properties, Property Yield = Net Property Income (NPI) from all properties/Total value of properties (based on the latest available valuation). This ratio is multiplied by 100 to deliver a percentage.

- This is in contrast to the Distribution Yield, which is the yield that the REIT investor receives.

Rental Reversion

- A metric captured by some REITs to show whether new leases signed have higher or lower rental rates than before.

Retail REITs

- REITs that hold properties such as shopping centres, malls, shopping arcades and other premises for retail activities.

RevPAR

- Revenue per Available Room is a metric used in the hospitality industry to measure the average amount of revenue a hotel makes per room.

- RevPAR = Hotel’s average daily room rate (ADR) x Occupancy Rate; Hotel’s total revenue from rooms available/Number of days being measured.

Risk Free Rate

- Amount of yield an investor will make if he invests in government-issued bonds. It is usually used as a benchmark to which the REIT dividend yield should be ahead of to attract investors.

Shari’ah Compliant REITs

- REITs that have committed to operate their businesses in line with the principles of Islamic jurisprudence. This includes complying with Shari’ah investment principles and procedures, for example, avoiding taking up tenants that are not aligned with these values like alcoholic beverage dealers, karaoke lounges, wine cellars and gambling premises.

Sponsor

- The sponsor is the party that typically sources the properties that are placed into the initial portfolio of the REIT and may continue to provide a pipeline of assets for the REIT. Usually, the sponsor also owns stakes in the REIT manager and the REIT.

Total Return

- The sum of a stock’s dividend income and its capital appreciation, before taxes and commissions.

Triple Net Lease

- A lease agreement where the tenant agrees to pay real estate taxes, property insurance and building maintenance costs, on top of monthly rentals and utilities.

- These agreements are generally beneficial to the REIT, as they are freed of the major operating costs of running the property.

Trust Deed

- A legal document setting out the details of a trust (e.g. identity of the trustee and manager, investment mandate) and the rights and obligations of unitholders

- Both business trusts and S-REITs are governed by their respective trust deeds with the trustee having full legal ownership of the trust’s assets instead of the trust’s unitholders.

Trustee

- The Trustee is responsible for holding the assets of the REIT on behalf of unit holders. Its duties are laid out in the trust deed for the REIT, which include ensuring compliance with all applicable laws, taking custody of the real estate assets, and protecting the interest of unit holders. The trustee is paid a fee for providing this service.

Unit Trust

- A unit trust is a fiduciary relationship in which one party, the trustee, holds legal title to property or assets for the benefit of unitholders of the unit trust, each of whom has an undivided share in the property or assets of the trust.

Weighted Average Lease Expiry (WALE)

- A metric used to measure the tenancy risk of a particular property. It is typically measured across all tenants’ remaining lease in years and is weighted with either the tenants’ occupied area or the tenants’ income against the total combined area or income of the other tenants using the following formula:

- Example:

- Tenant 1: Occupies 10% of rentable area (lease expires in 5 years)

- Tenant 2: Occupies 70% of rentable area (lease expires in 6 years)

- Tenant 3: Occupies 20% of rentable area (lease expires in 3 years)

- The WALE is therefore = (0.1 x 5) + (0.7 x 6) + (0.2 x 3) = 5.3 years